Data Center Infrastructure at Scale

AI and cloud demand are reshaping data center infrastructure at an unprecedented scale and speed, understanding their scale is crucial for future deployments.

This article is a collaborative effort by Peter Hirschboeck and Lisa Nguyen, representing views from impactECI.

The data center sector is undergoing a transformative shift in both scale and cost structure, driven by the exponential rise in AI workloads, expanding cloud computing, and rising sustainability expectations. With global electricity demand from data centers projected to double by 2030, and capital requirements surpassing $7.9 trillion, stakeholders must recalibrate their strategies. Meeting this challenge will require coordinated investment, innovative engineering, and deep utility-sector collaboration to ensure grid reliability, capital efficiency, and long-term competitiveness.

The physical scale and pace of deployment are unprecedented

U.S. data centers currently operate more than 20 GW of capacity1, with demand projected to reach 35 GW by 2030 as AI, cloud, and high-performance computing accelerate2. This rapid expansion is reshaping infrastructure needs across power, land, water, and labor.

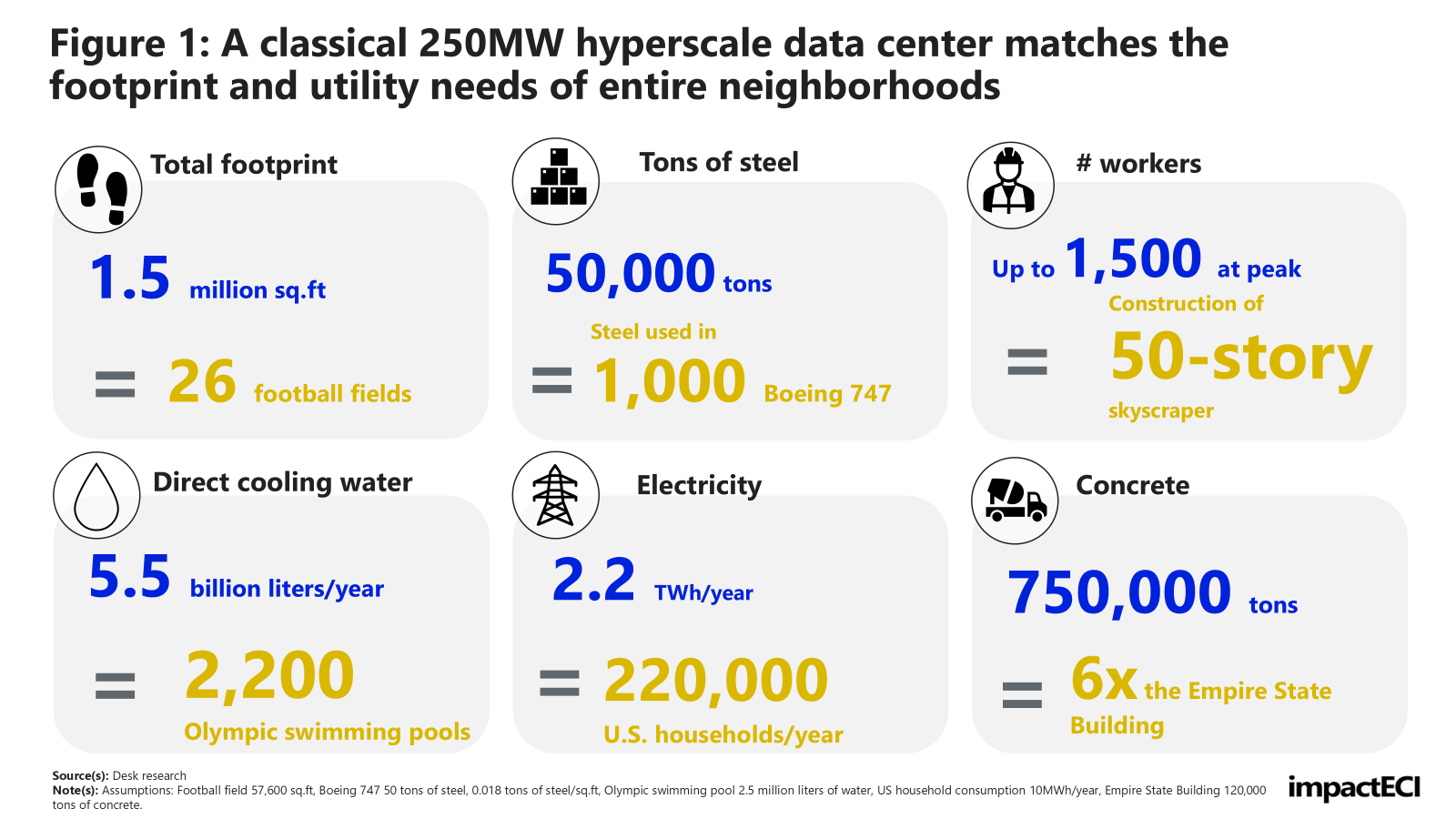

Bigger footprint, higher densities: A conventional hyperscale data center delivering 250 MW of capacity typically spans 1.3 to 1.5 million sq. ft for single-story building space3, roughly equivalent to 23-26 football fields, though some may be larger. An AI-optimized facility, by contrast, may require up to 30% less space, enabled by compact architectural layouts, advanced cooling systems, and ultra high-density server racks4. While both facilities draw enough electricity to power more than 220,000 U.S. homes, the AI-optimized site delivers this on a much smaller footprint, requiring significantly higher electrical and cooling capacity/sq. ft, which heightens site selection and permitting complexity.

Material intensity is equally significant: Steel remains a foundational material in data center construction. A traditional 250 MW, 1.5 million sq. ft single-story facility typically requires up to 50,000 metric tons of steel, equivalent to the steel in 1,000 Boeing 747s (roughly 50 tons/aircraft)5. Facilities require an estimated 0.014 to 0.018 metric tons/sq. ft6 of building space, driven by the demands of structural framing, cooling systems, and heavy equipment support. Complementing this is the use of 500 to 1,000 cubic meters of concrete/MW, translating to ~ 750,000 metric tons of concrete per facility or more than six times the volume used in constructing the Empire State Building7, underscoring the industrial scale of hyperscale buildouts. By contrast, the adoption of liquid cooling in AI-optimized data centers requires additional stainless-steel components for piping, manifolds, and structural supports, further increasing steel usage per square foot. Embodied carbon per sq. ft or per MW is materially higher in AI-optimized designs8, amplifying ESG exposure and complicating project approval in carbon-sensitive jurisdictions .

Cooling drives notable water consumption: Data center water usage effectiveness (WUE) for evaporative cooling can be as high as 2.5 cubic meters/MWh or 2,500 liters/MWh of IT load, depending on the type of evaporative cooling equipment, local climate, and the choice of server cooling technology9. A 250 MW site using evaporative cooling may use up to 15 million liters/day just for cooling, enough to fill 6 Olympic pools daily, totaling the annual needs of ~2,200 Olympic pools. In contrast, advanced direct-to-chip liquid cooling systems can reduce water usage10 by up to 92%, offering a critical lever for operators in water-stressed regions or jurisdictions with strict environmental permitting requirements.

Labor requirements are front-loaded: Construction phases of 250 MW scale often involve 1,000–2,000 workers, comparable to the labor needed for building a 50-story skyscraper. However, once operational, automation enables lean staffing, with typically fewer than 100 full-time employees required on-site.

Global capacity and growth outlook: Global data center capacity is on a sharp upward trajectory. In 2025 alone, over 10 GW of new capacity is expected to break ground, driven by hyperscaler expansion, ongoing cloud migration, and AI deployments. According to IEA projections, total electricity consumption from data centers is expected to nearly double, reaching 945 TWh by 2030, equivalent to the annual output of ~ 120 standard 1GW nuclear reactors operating at 90% capacity factor. Addressing this growth will require accelerated investment in transmission, grid interconnection, and permitting reform.

Global capacity and growth outlook: Global data center capacity is on a sharp upward trajectory. In 2025 alone, over 10 GW of new capacity is expected to break ground, driven by hyperscaler expansion, ongoing cloud migration, and AI deployments. According to IEA projections, total electricity consumption from data centers is expected to nearly double, reaching 945 TWh by 2030, equivalent to the annual output of ~ 120 standard 1 GW nuclear reactors operating at 90% capacity factor. Addressing this growth will require accelerated investment in transmission, grid interconnection, and permitting reform.

Cost structure: A capital-intensive model under pressure

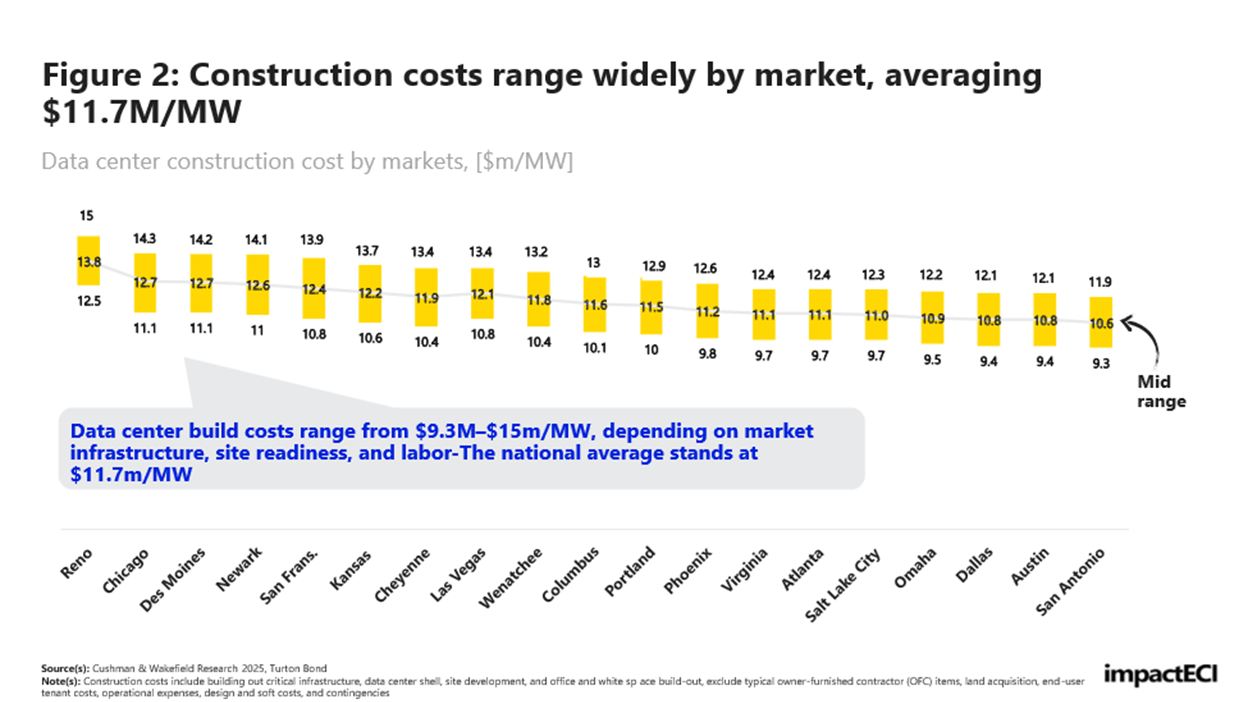

Building a hyperscale data center is among the most capital-intensive infrastructure projects today: Depending on location, design specifications, and technology configurations, construction costs range from $9.3 to $15 million/MW or $600 to $1,100/sq. ft11. A 1.5 million sq. ft, 250 MW facility in Reno, Nevada may exceed $3.7 billion in upfront cost . On average, 53% of total construction cost is attributed to building out critical infrastructure, including switchgear, chillers, CRAHs, UPS systems, copper wiring, etc. The remaining cost is distributed across the data center shell (21%), site development (10%), and office and white space build-out (16%)12. These estimates exclude typical owner-furnished contractor (OFC) items, land acquisition, end-user tenant costs, operational expenses, design and soft costs, and contingencies.

Globally, total capital investment for AI-ready data centers could reach $5.2–$7.9 trillion by 2030-the higher end nearly doubles the GDP of Germany or Japan in 2024.

Grid access, not acreage, is becoming the key lever in land valuation: As transmission queues grow and grid congestion intensifies, the ability to secure MWs, not just acres, is rapidly becoming the defining factor in site selection and project economics. According to Cushman & Wakefield's report, standard U.S. data center-zoned land averaged $6/sq. ft (~$266,000/ acre) between 2022-2024. However, powered land sites with existing electrical infrastructure can command a 3–4x premium (~$800,000/ acre)13 due to their ability to accelerate time-to-market. This pricing premium reflects the value of faster time-to-market, reduced permitting risk, and guaranteed grid access. By contrast, non-powered land, ranging from $5,000- $20,000/acre14, requires major transmission upgrades, rendering it impractical for near-term deployment. As developers compete for grid-adjacent parcels, powered land is becoming a critical determinant of site viability and overall project economics.

Operating costs are rising and cooling technology is now a key differentiator

As data centers scale, ongoing OpEx has become a critical component of total cost of ownership. For hyperscale deployments, annual operating costs typically range from $200,000-$400,000/MW15 of IT load, or roughly $50 million to $100 million for a 250 MW facility. AI and high-performance computing (HPC) data centers tend toward the higher end of this range, driven by elevated power densities, intensive cooling requirements, and more robust electrical and mechanical systems. General-purpose hyperscale sites typically operate closer to the lower end. Across this footprint, energy consumption accounts for 60–70% of total OpEx, with this share rising further in AI environments due to sustained GPU utilization and greater thermal load. As a result, efficiency-focused innovations, particularly in cooling technologies, have become pivotal to preserving margins and ensuring scalability16.

Cooling technologies are reshaping energy and water intensity

The choice of cooling architecture plays a pivotal role in determining operating efficiency. Evaporative cooling systems typically consume 3.5 to 4.5 MWh/kW17 of IT load annually, trading higher water use for moderately lower electricity costs. In contrast, direct-to-chip liquid cooling significantly reduces water consumption while enhancing thermal performance, lowering annual energy use by approximately 18 percent to 2.8–3.7 MWh/kW of IT load, depending on workload density. As electricity prices and input costs rise, particularly in primary data center markets, operational efficiency and thermal design are emerging as decisive levers for margin protection and long-term competitiveness.

Key cost and growth drivers

The rapid evolution of AI is fundamentally reshaping energy consumption and infrastructure requirements. AI queries consume up to 10 times more electricity than traditional cloud searches18. As generative AI and foundation models scale, data center-related electricity demand could create a 15+ GW supply deficit in the U.S. by 2030 if left unaddressed.

Next-generation cooling systems (e.g., liquid cooling), enhanced power redundancy, and ultra-low latency networking are no longer optional19, they are necessary for AI-ready environments. These technologies improve performance but add to both capital and operational cost profiles. Engineering firms and operators must rethink design standards to support modular, high-density computing with lower environmental impact.

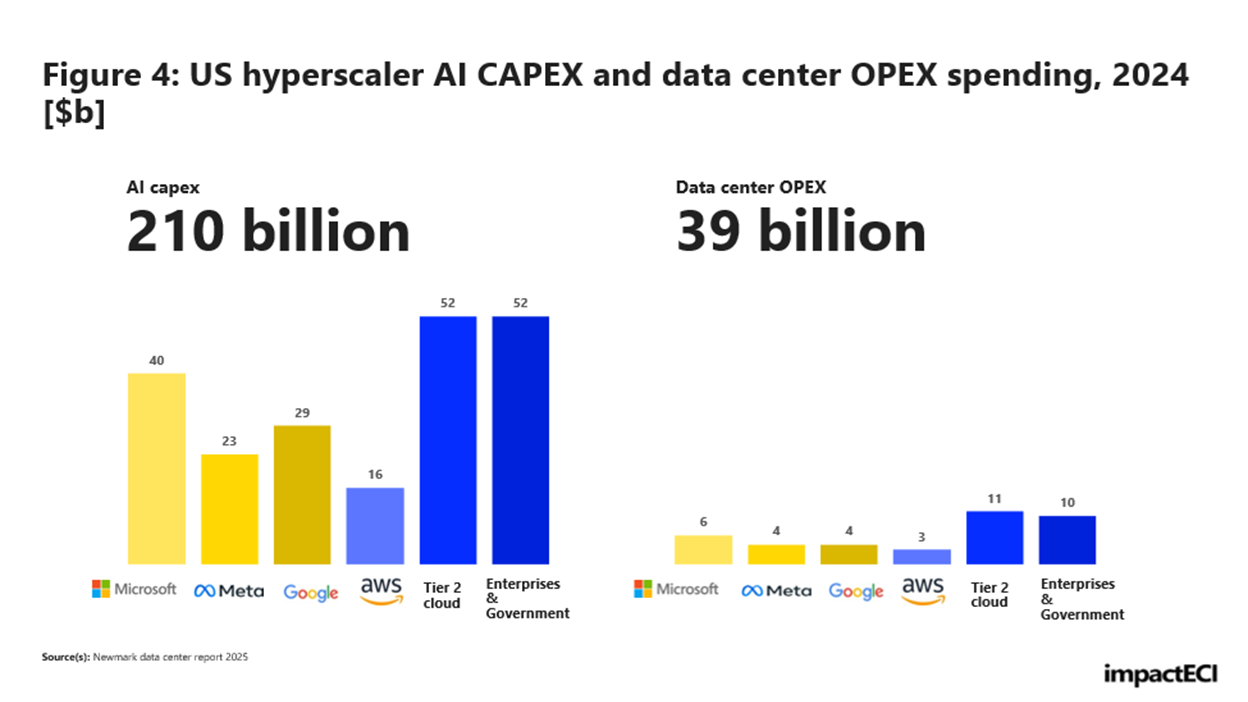

Meeting future demand will require unprecedented levels of financing. In 2025 alone, $170 billion in new data center asset value will need to be financed, most of it structured as 65–80% loan-to-cost20. As private equity, infrastructure funds, and institutional investors enter the data center space, competition for capital is expected to intensify, elevating the importance of risk-adjusted returns and lender confidence in project economics.

Strategic implications across the value chain

For investors: The capital requirements for AI and cloud-driven data centers present both opportunity and risk. While asset trading volume remains modest today, the scale of upcoming development, paired with financing intensity, requires a reassessment of valuation benchmarks, return timelines, and macro exposures. Investors must also weigh regulatory, grid interconnection, and ESG-related constraints that may impact permitting and project execution.

For utilities: With U.S. data center demand expected to reach 35 GW by 2030, utilities face mounting pressure to expand grid capacity, streamline interconnection timelines, and adopt more sophisticated forecasting tools. Coordinated planning between utilities and hyperscale developers will be essential. Particularly in high-growth regions like Northern Virginia, Dallas, and Phoenix, where congestion and capacity constraints are already evident.

For developers and off-takers: Energy strategy is becoming a competitive differentiator. As demand accelerates, data center developers, such as Vantage and EdgeCore, must place greater emphasis on site selection, energy sourcing, and sustainability performance. Power availability and pricing will shape long-term competitiveness, while off-takers such as AWS and Microsoft must build capabilities to manage demand flexibility, implement renewable procurement strategies, and meet increasingly stringent emission reporting requirements. With data centers projected to consume up to 12% of total U.S. electricity by 2030, ESG compliance is no longer optional; it is strategic. Regulatory scrutiny and societal expectations are intensifying, particularly around scope 2 (electricity usage) and scope 3 (supply chain) emissions. Operators that lead in transparency and decarbonization will be better positioned to secure permits, attract customers, and unlock capital.

Conclusion: Planning for scale in the AI era

Data centers are now among the most capital -and energy- intensive infrastructure categories. Their scale rivals airports, hospitals, and even grid substations. As generative AI, edge computing, and digital transformation reshape demand profiles, success will require a multi-stakeholder strategy. Utilities, developers, investors, and regulators must coordinate with greater urgency, agility, and technical sophistication.

Those who lead will help build the digital backbone of the 21st century, one that is scalable, resilient, and aligned with a low-carbon future.

For more information, reach out to hello@impactECI.com

The views and opinions in these articles are solely of the authors. They are offered to stimulate thought and discussion and not as legal, financial, accounting, tax or other professional advice or counsel.

https://uptimeinstitute.com/resources/research-and-reports/uptime-institute-global-data-center-survey-results-2023

https://restservice.epri.com/publicdownload/000000003002030643/0/Product

https://www.webopedia.com/technology/10-biggest-data-centers-in-the-world/

https://www.applieddigital.com/insights/different-by-design-how-applied-digital-is-redefining-data-center-infrastructure

https://aviation.stackexchange.com/questions/12958/what-materials-make-up-most-of-the-weight-of-an-aircraft

https://datacentremagazine.com/articles/the-role-of-steel-in-todays-data-centre-industry

https://www.ascemetsection.org/committees/history-and-heritage/landmarks/empire-state-building

https://arxiv.org/pdf/2403.04976v2

https://blog.equinix.com/blog/2024/11/13/what-is-water-usage-effectiveness-wue-in-data-centers/

https://www.datacenterknowledge.com/cooling/why-liquid-cooling-is-essential-to-the-future-of-data-centers

https://cushwake.cld.bz/Data-Center-Development-Cost-Guide-2025

https://cushwake.cld.bz/Data-Center-Development-Cost-Guide-2025

https://cushwake.cld.bz/Data-Center-Development-Cost-Guide-2025/12-13/

https://cushwake.cld.bz/Data-Center-Development-Cost-Guide-2025/12-13/

https://www.byteplus.com/en/topic/385970?title=how-much-does-a-100-megawatt-data-center-cost

https://betterbuildingssolutioncenter.energy.gov/better-buildings-progress-report

https://citeseerx.ist.psu.edu/

https://www.iea.org/reports/energy-and-ai

https://www.ahead.com/resources/liquid-cooling-is-not-new-but-now-its-necessary/